Shareholder first half update

A message from ANZ's Chairman - Paul O'Sullivan

A message from ANZ's Chairman - Paul O'Sullivan

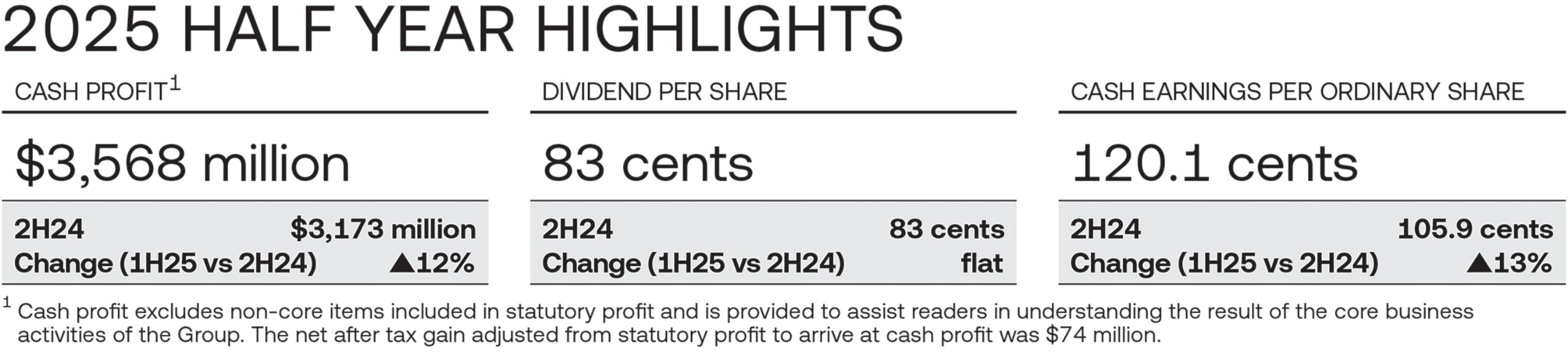

ANZ reported a good result for the half year ended 31 March 2025, driven by continued momentum across each of our divisions and the inclusion of Suncorp Bank. Our cash profit was $3.6 billion, up 12% from the previous half.

Our Interim Dividend of 83 cents per share, partially franked at 70 per cent, held steady from the previous half and returned $2.5 billion to you, our shareholders.

Importantly, you can see the ongoing benefits of a well performing, diversified portfolio in this result.

Performance

Through the half we delivered our highest cash earnings per share outcome since the first half of 2023 and our return on equity increased by almost 100 basis points to 10.2 per cent.

Costs continued to be well managed even as we have maintained strong levels of investment in our business over a number of years to fuel growth and efficiency. Since 2019 we have successfully delivered $1.9 billion in cumulative productivity savings, demonstrating that productivity remains a core strength of your bank.

Banking loans and deposit volumes were both up 3 per cent in the half, with all Divisions contributing. We also saw continuous improvements in capital efficiency during the half and our capital position remained strong, with a Common Equity Tier 1 (CET1) Ratio of 11.8%.

ANZ completed $1.2 billion of the previously announced on-market share buyback. Given increased uncertainty in the macro environment, we believe it is appropriate to adopt slightly more conservative capital settings, including retaining the flexibility to adjust the pace of the remaining share buyback if needed. This is something that we will keep you updated on going forward.

Suncorp Bank

Suncorp Bank reported a strong underlying performance relative to its regional peers. Importantly, the completion of the acquisition is helping us bolster our presence in Queensland and strengthen our Retail and Commercial businesses for the long term.

Non-Financial Risk

Disappointingly, you may have seen during the first half that important concerns were raised by our regulators around ANZ’s risk culture and non-financial risk management practices.

An independent review into these areas within our Global Markets business found a series of shortcomings, and made it clear there is significantly more work to be done in this regard. The review did not find evidence of widespread or systemic misconduct.

ANZ is committed to addressing the issues raised and has accepted all 19 recommendations and 53 sub-recommendations from the review.

ANZ also entered into a Court Enforceable Undertaking (CEU) with the Australian Prudential Regulation Authority (APRA) relating to non-financial risk management practices and risk culture across the Group. This included the application of a further $250 million capital overlay, bringing the total capital overlay related to non-financial risk to $1 billion.

The Board and management are disappointed that we have not met APRA’s non-financial risk management and risk culture expectations, and we are firmly committed to ensuring we meet and exceed these standards.

Supporting our customers

Reflecting on the first half, the cost of living remained a challenge for many of our retail and small business customers. Encouragingly, there are signs that interest rates may continue to come down during the remainder of the year, providing some relief for households and businesses.

However, we know that times are tough for many and our team is committed to supporting our customers as they navigate their specific circumstances.

Welcoming Nuno Matos

I am pleased to welcome Nuno Matos, an international banker with more than 30 years of extensive experience, as ANZ Group’s new Chief Executive Officer.

Having worked across nine global markets, I am confident that his proven ability to run retail and wholesale banks while also overseeing bank integrations and migrations makes him an outstanding choice as our new CEO.

I would like to take this opportunity to pay tribute to outgoing CEO Shayne Elliott, who has been at the helm since 2016.

During his tenure, Shayne successfully delivered the acquisition of Suncorp Bank and transformed the Group, including by selling non-core assets and investing in leading technology platforms to underpin growth. He leaves an important legacy and strong starting point for Nuno.

Finally, I would like to acknowledge our people at ANZ for their tireless work during the year. Their countless individual contributions over the half combined in a group-wide effort that ensured we helped more of our customers achieve their financial goals.