The technology super cycle is providing economies across Asia, outside China and India, a level of immunity from the uncertainty surrounding the Middle East conflict, helping the region overcome inflation and the accompanying tightening of monetary policy.

As a result, ANZ Research has lifted its 2026 gross domestic product (GDP) growth forecast for Asia (ex-China, India) to 4.7 per cent from 4.2 per cent.

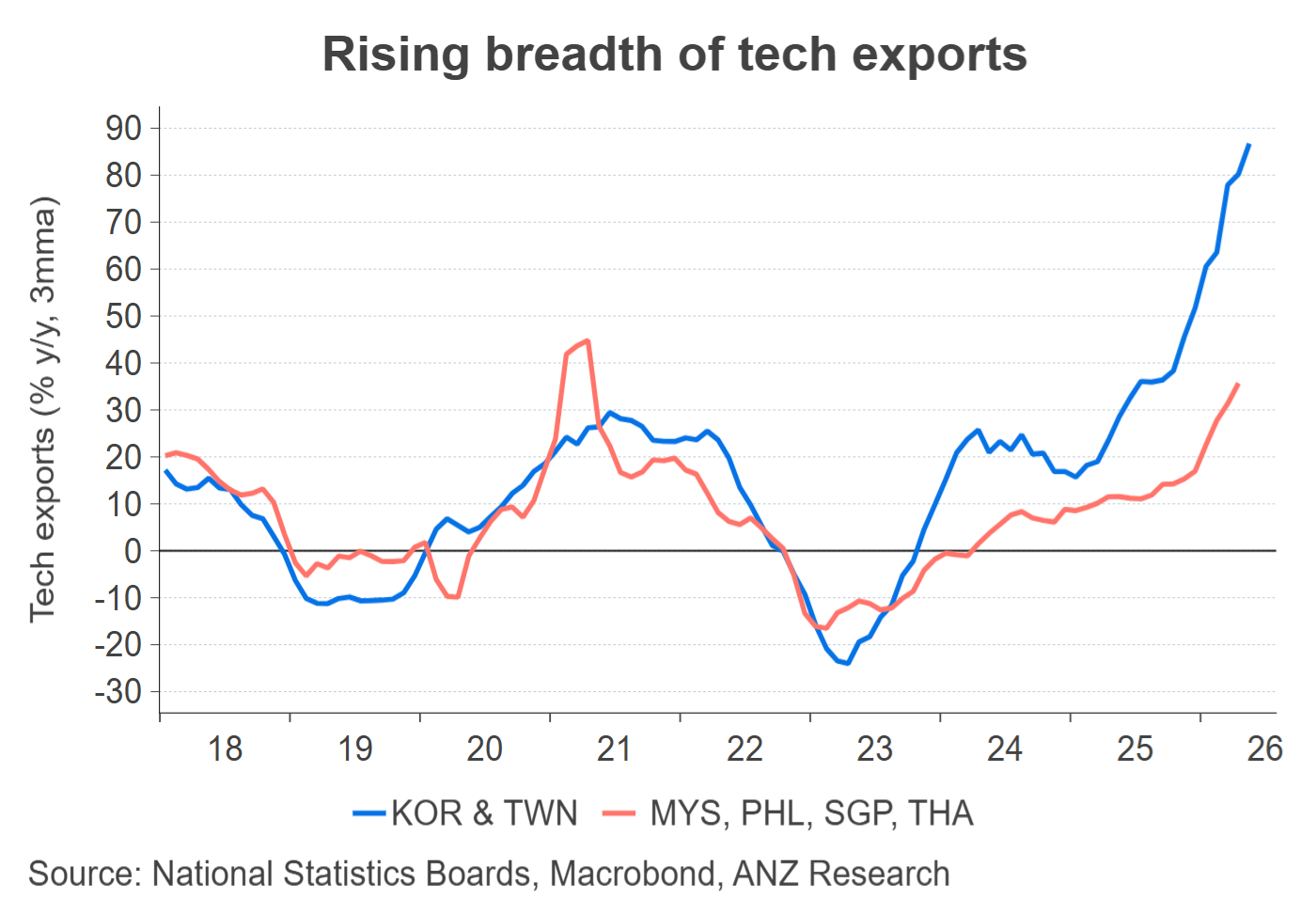

The upward revisions are concentrated in economies with significant exposure to the tech cycle: Malaysia, Singapore, South Korea and Taiwan, where tech exports are not only growing at an unprecedented pace but are also starting to lift plant and equipment investment.

In Thailand, the ongoing construction of artificial-intelligence data centres has sharply reversed the trend of stagnant investment, but the related transitory deterioration in ‘net exports’ warrants a mild downgrade to the 2026 GDP growth forecast from 2.4 per cent to 2.2 per cent.

Looking ahead, more demanding base effects may slow annual export growth rates. However, this should not be interpreted as a weakening of the tech cycle — the projected 36 per cent increase in projected capital expenditure by US hyperscalers should sustain the region’s exports in level terms for a prolonged period.

However, the trickle down to household consumption is uneven. Consumer sentiment has generally softened, reflecting both direct and second-round effects of higher energy prices. Fiscal support should provide a partial buffer.

In contrast, ANZ Research has downgraded growth forecasts for both Indonesia and the Philippines. Despite Indonesia’s stronger-than-expected first-quarter outturn of 5.6 per cent, year on year, ANZ Research expects the full-year 2026 will average 5.0 per cent, reflecting a shift towards more conservative fiscal policy.

The surge in public consumption (up 21.8 per cent year on year) in the first quarter lifted household consumption to 5.5 per cent, above its long-term average, but this impulse is unlikely to persist. Bank Indonesia’s tightening cycle will also become a drag on growth, although a mild one given low household and corporate leverage.

The Philippines’ outlook is more constrained by weak household and business confidence, elevated inflation and higher interest rates. Public spending likely bottomed in the first quarter, but a material recovery is unlikely until governance issues surrounding infrastructure projects are fully resolved.

Likely to intensify

So far, inflation has exceeded official targets only in the Philippines, South Korea and Vietnam. However, the uptrend is likely to intensify in the coming months.

This view is based on three considerations.

The first is the need to overcome margin compression. Corporates have been absorbing higher input costs, which is evident in declining consumer and producer price index readings, and output-input price ratios in manufacturing purchasing managers’ indexes.

The second is rising dispersion of price pressures in the inflation basket. And the final factor is emerging food price pressures, driven by higher fertiliser prices and El Niño-related dry weather conditions.

Second-round effects of higher energy prices will also take time to unwind, despite the recent moderation in crude oil prices.

Aligned

Fiscal and monetary policy in the region are aligning to address inflation. On the fiscal side, many economies have expanded energy subsidies and broader welfare support, amounting to 1.1 per cent of GDP in South Korea and Thailand and 0.4 per cent in Malaysia. The Philippines stands out with negligible fiscal support, reflecting tight fiscal constraints and legal rigidities in fuel and utility pricing.

ANZ Research does not expect a material overshoot of 2026 budget deficit targets, as higher subsidy outlays are likely to be compensated by lower public capital spending in most economies. As a result, the net fiscal impulse is becoming less supportive of growth, though this is likely to be offset by the region’s extraordinary export cycle.

South Korea and Thailand are exceptions. South Korea’s stronger-than-budgeted tax collections allowed for a supplementary budget without recourse to additional borrowing. The Thai government plans to expand off-budget borrowing by around 2 per cent of GDP to support targeted welfare transfers and renewable energy investment. ANZ Research does not expect these additional borrowings to crowd out the private sector, as private sector demand for funds remains mild.

Course clear

Amid rising inflation and secure growth, the course of monetary policy is clear. Only three central banks have tightened monetary policy so far, but ANZ Research expects others to start hiking rates from the next quarter.

Incrementally, the State Bank of Vietnam is likely to be aggressive, with two hikes of 50 basis points each. Bank Negara Malaysia is likely to reverse last year’s cut of 25 basis points, as inflation should remain contained by extensive subsidies.

Indonesia and the Philippines are unique in the current tightening cycle as their monetary policy dynamics are not backed by strong growth. Indonesia’s currency weakness and investor concerns over broader macro policies warrant further tightening. Depending on how rupee stability evolves, ANZ Research forecasts two to four rate hikes of 25 basis points each.

The Philippines’ central bank is focussed on alleviating inflation despite sub-par growth of 2.8 per cent year on year in the first quarter. ANZ Research expects two more rate hikes of 25 basis points each, translating into a cumulative trough to peak tightening of 100 basis points.

External balances remain broadly manageable, except for Indonesia and the Philippines. Indonesia’s first-quarter current account deficit of 1.1 per cent of GDP is likely to be replicated for the remainder of 2026, with the overall balance of payments (BoP) remaining in deficit for the second consecutive year.

Other than current accounts, stagnating foreign direct investment and volatile portfolio flows are straining the overall BoP. The BoP problem is more acute in the Philippines where the 2026 current account deficit is officially forecast at 4 per cent.

Thailand’s current account deficit widened to a multi-year high of $US7.6 billion in April, driven by higher energy and capital imports and weaker tourism inflows. But strong forex reserves are likely to provide resilience and absorb a temporary deterioration in the current account balance.

Sanjay Mathur is Chief Economist, Southeast Asia and India at ANZ Research

This is an edited excerpt from the ANZ Research report “ANZ Research Quarterly: crisis legacies”, published June 23, 2026.