Digital assets could provide the basis for a redesigned Australian superannuation payments system – one that could help the country’s proposed payday super initiative bring forward returns for members and increase productivity in the industry.

Australia’s roughly $A3.5 trillion super industry is a critical plank of the nation’s economy. For business, ensuring those funds make their way to members hasn’t always been easy. In fact, in some cases, the process can be a painful one.

From July 2026, proposed new super rules would see that process shift from a quarterly cadence to one tied to payroll, meaning many employers would need to pay employees their super on payday. This would increase pressure on businesses to get it right, and fast, as the implications of errors or missteps can be significant – and costly.

Technology can help the process, and the rate of change in payments around the world is testament to that. But making a complex process faster doesn’t always solve all its issues. There’s a real opportunity to reimagine the process and simplify it entirely.

ANZ has been experimenting with industry participants on solutions that can demonstrate that opportunity. Earlier in 2023, ANZ helped process live contributions as part of the of the Reserve Bank of Australia and Digital Finance Cooperative Research Centre central bank digital currency (CBDC) Pilot.

From that work, it’s clear to ANZ that digital assets provide the opportunity to deliver employers immediate pre-payment validation to member accounts in a way that is transparent, efficient and safe. Such benefits create simplification for employers and funds, as well as better outcomes for members – positioning the superannuation sector for the digitised economy of the future.

Better

The Australian government’s proposed new super rules hope to create better retirement outcomes for members. Announced earlier in 2023, the changes are aimed at helping members that are underpaid, receive money late or don’t receive contributions at all.

The challenge is large. The Australian Tax Office estimates 4.9 per cent of super was not paid in fiscal 2020 - roughly $A3.4 billion.

For members of funds, any adoption of digital assets as a payment option might seem invisible, but would greatly improve both the user experience and financial outcomes in retirement.

Australian employers paid roughly $A114 billion in super to members in fiscal 2022. However, the current process means those funds spend a lot of time idle, not generating returns for members. There is appetite to ensure funds going through the system reach employees in a timelier manner, with the right information to allocate the investment.

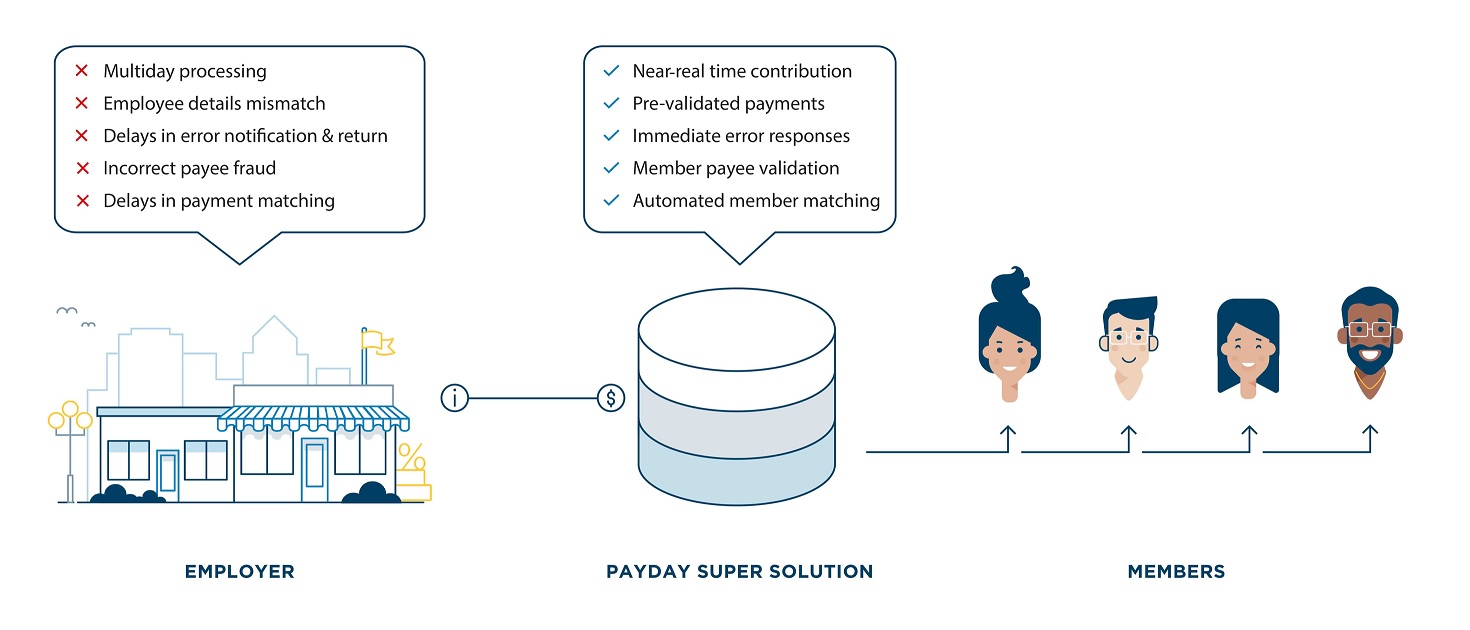

Digital assets could speed up the process by shifting the account validation process to before, rather than after the payment is made. This secure and transparent process can ensure the allocation happens in seconds.

Results from ANZ's work on the RBA and DFCRC’s CBDC pilot demonstrate the opportunity for members to gain immediate feedback or visibility of their super being received on payday, not only investing it earlier as a result, but validating their employer has fulfilled their obligations.

Rush

For many businesses, the current system is not always a clean process, and can sometimes devolve into a mad rush in the days leading up to the quarterly payment deadline. A lot of information is required when passing on contributions and there is no immediate response that payments have been successfully received.

Payment-matching errors during this time - sometimes due to detail mismatches, deactivated member accounts or even fraud - can extend the timeline further and add to the sense of panic for employers, given the consequences of late or incorrect payments. These kinds of errors are not uncommon.

Mistakes can be costly. Employers face hefty penalties under the superannuation guarantee of up to 200 per cent of the original super amount, with other fees, interest and tax implications on top. By mid-2026 under the proposed changes, businesses that execute payroll fortnightly would face the prospect of this ordeal a lot more than four times a year.

Employer contributions powered by digital assets could streamline this process, reducing administrative burden and providing immediate responses to errors. The technology promotes efficiency in compliance by assisting employers to meet contribution deadlines and regulatory requirements, ultimately saving time, money and stress for businesses that would take confidence their employees are receiving contributions.

For employers, digital assets can improve the payday experience as member details and accounts are validated prior to payment.

Built-in payee identification helps protect the employer from fraudulent payments and creates an immediate feedback response that can traditionally take days. Payment errors can be found and fixed on the spot. Under the current system, it can take days for errors to even be reported.

Through the current process, it can take anywhere between three to 15 days for contributions to get to a fund. Using digital assets can help make this happen in near real-time.

Superannuation funds are another key stakeholder that would benefit from a shift to a digital-asset-based system. The use of smarter payments could help modernise operations, moving payments and information together on a common ledger that automates the matching of members and their details. This would help both the funds application process and the ability for administrators to allocate funds for investment.

For members, the transparency and automation can also support visibility of contributions as they happen, providing trust in the system and confirmation that employers are meeting their obligations.

Practice

There’s no doubt the sector will look to respond to the 2026 super proposals with improved payment methods like PayTo, and many organisations are in support of such a shift. While such a move would be an improvement in payments, in its current state it would not solve some of the issues experienced today.

At ANZ, we’re thinking deeper about the future. In October, a group of industry participants teamed together as part the RBA CBDC pilot to test our ideas around digital assets and how moving payments and information together benefits superannuation.

Along with several superannuation funds - including large, high-profile groups - and one self-managed fund, ANZ worked on a project to successfully deliver members near real-time employer contributions, reducing potential for fraud and counterparty risk and increasing the efficiency of the system. The pilot successfully demonstrated the effectiveness of digital assets in solving these issues and the potential for broader-scale application.

The solution helped address limitations in the existing system that caused many of the delays in contributions. It also demonstrated the benefits of pre-validation of accounts and how matching can be improved by moving the information and the payment together.

The work showed, through collaboration and by reimagining the process, that the superannuation sector can leverage modern technology to solve the problems of today - and tomorrow.

Opportunity

Australia’s Treasury and the Australian Tax Office (ATO) are currently consulting participants within the industry on the implementation of the proposed rules. ANZ has engaged on these discussions. With a significant amount of payment innovation and employers now largely using payroll software, there is a unique opportunity to solve problems in the system that were previously not possible to fix.

At ANZ, we believe this approach represents a unique chance to do things better for the benefit of members, superannuation funds and employers.

The bank is invested in the future of the industry and believe digital assets and smart contracts will play a fundamental role in the future of payments and the digital economy.

Tweaking around the edges might be easy now, but as an industry, we can’t afford to miss the opportunity to reimagine the future of superannuation contributions – a future that members, employers and superannuation funds deserve.

Jason Hunt is Executive Director, Industry and Innovation at ANZ Institutional