-

New Zealand’s economy is recovering, although the road ahead is still highly uncertain. Supply chain disruptions continue to create challenges moving goods around the world.

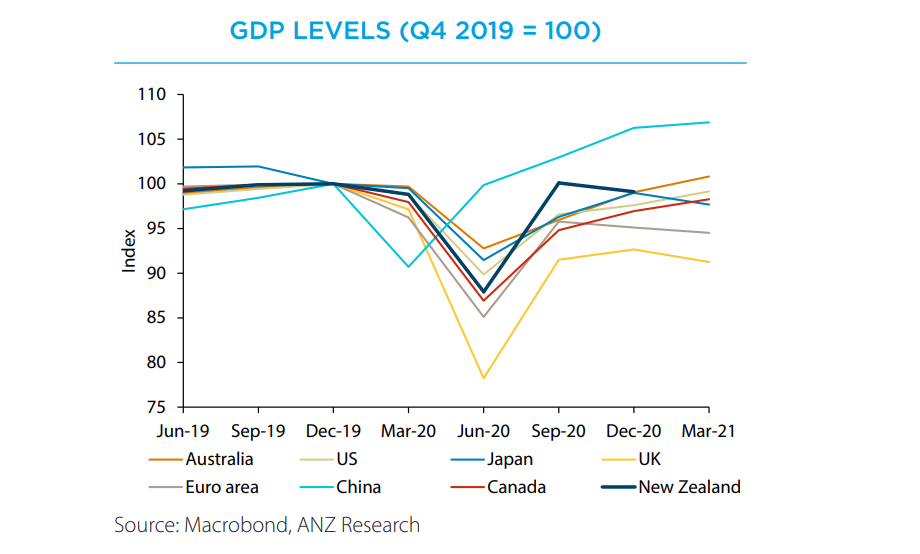

New Zealand is one of the best-performing economies among its key trading partners primarily because it had success eliminating and keeping out COVID-19 due to its isolation and tight border controls.

Much of the NZ economy is back operating at full steam, largely making up for the sectors still lagging. The change brought about by the pandemic was very abrupt, and altered both the level and the composition of spending in NZ and overseas.

Consumption globally has been bolstered by an unprecedented amount of temporary fiscal support. With many economies locking down, people have naturally traded restaurant/experience/travel spending for purchases of more stuff, including online.

This compositional shift towards manufactured goods was unexpected and abrupt, and it’s creating significant headaches for global supply chains, seeing shipping costs lift – significantly.

In time

Supply chain disruption is challenging the world’s ‘just-in-time’ approach, a dominant feature of global trade these past few decades. Reduced air cargo means there’s more for ships to carry, and port congestion mean ships are spending too much time sitting idle.

How long these disruptions persist is anyone’s guess, but global inventories will eventually be rebuilt (and possibly kept permanently higher) and supply chains ironed out.

That could happen as soon as the end of this year but more likely the supply challenges will persist well into 2022.

As cost pressures unwind NZ should see inflation pressures ease both locally and around the globe, which is why policymakers are looking through inflationary pressure for now. There is no doubt the NZ economy has performed much stronger than anyone dared hope.

Much of the strength economy can be attributed to a handful of key factors. Among them, a successful containment of COVID-19, which has provided kiwis the freedom and confidence to go out – and spend.

Additionally, fiscal policy stepped up to the plate, essentially putting a healthy chunk of the second quarter’s lost production on NZ’s balance sheet - largely via the wage subsidy – which meant incomes did not fall anywhere near as much as production GDP did.

Finally, low interest rates stimulating the economy – admittedly largely via housing, as opposed to business investment.

Economic growth is expected to remain subdued through 2021 but pick up in 2022 as global economies improve and fewer border restrictions allow growth in sectors of the economy that are severely stifled at present, such as tourism and foreign education.

Cost pressures associated with the supply disruption are expected to eventually dissipate and give way to a demand-driven lift in inflation. This will be driven by a tightening of other resources including labour and natural resources

Helping out

The combination of monetary policy support and fiscal stimulus has provided a significant cushion to the economy, which has helped facilitate the vigorous bounce-back seen to date.

On the monetary side, the RBNZ, cut the official cash rate to a record low, implemented new asset-purchasing and lending programs, program, and prepared the banking system for negative interest rates if required.

On the fiscal side, stimulus has been most potent from the wage subsidy, which protected jobs and incomes and provided a degree of certainty during disruption, albeit at enormous cost. A range of other temporary policy supports accompanied it.

Now that the wage subsidy has rolled off, fiscal policy is pivoting towards the likes of infrastructure spending, which will support the level of economic activity.

Overall, monetary and fiscal policy settings are expected to be expansionary for a while yet. ANZ Research expects the RBNZ will maintain a cautious approach to removing stimulus in line with their least-regrets approach.

Policy normalisation will be a gradual, multi-year process. The RBNZ is forecasting they will start lifting the OCR in August 2022, which is consistent with ANZ’s forecasts. Risks are skewed to this being a little earlier, but the RBNZ will want to wait for the data to settle before kicking off a tightening cycle.

Assuming no dramatic developments in terms of COVID or global financial markets, wage growth and inflation expectations are the key data to watch in terms of the medium-term inflation outlook and therefore the likely path for the OCR and interest rates more generally.

Susan Kilsby is an Agriculture Economist and Sharon Zollner is Chief Economist NZ at ANZ

This story is an edited version of an ANZ Research note. You can read the original note HERE.

Share

Related articles

-

China faces a new economic normal as policymakers look to maintain growth in the economy.

2024-10-23 00:00 -

Three key elements have put the India’s economic destiny is in its own hands.

2024-10-03 00:00 -

Ahead of Sibos in Beijing, Raymond Yeung runs through the themes that will shape the global economy in 2025.

2024-10-14 00:00

This publication is published by Australia and New Zealand Banking Group Limited ABN 11 005 357 522 (“ANZBGL”) in Australia. This publication is intended as thought-leadership material. It is not published with the intention of providing any direct or indirect recommendations relating to any financial product, asset class or trading strategy. The information in this publication is not intended to influence any person to make a decision in relation to a financial product or class of financial products. It is general in nature and does not take account of the circumstances of any individual or class of individuals. Nothing in this publication constitutes a recommendation, solicitation or offer by ANZBGL or its branches or subsidiaries (collectively “ANZ”) to you to acquire a product or service, or an offer by ANZ to provide you with other products or services. All information contained in this publication is based on information available at the time of publication. While this publication has been prepared in good faith, no representation, warranty, assurance or undertaking is or will be made, and no responsibility or liability is or will be accepted by ANZ in relation to the accuracy or completeness of this publication or the use of information contained in this publication. ANZ does not provide any financial, investment, legal or taxation advice in connection with this publication.