-

The current momentum of the tech cycle is likely to be sustained through 2021 and most of 2022. As a result, tech exports will support and drive Asia’s recovery through this period.

The upswing is being driven by a combination of booming demand and supply shocks related to the pandemic, as well as innovation and technological breakthroughs.

The longevity of each of these factors differ wildly. The pandemic-led demand boost is a one-time expansion. The supply situation is a medium term issue and will play a significant role in supporting the tech cycle through 2021 and part of 2022.

The technological breakthroughs are fundamental shifts in the tech cycle which will guide its course over the medium to long term.

Demand

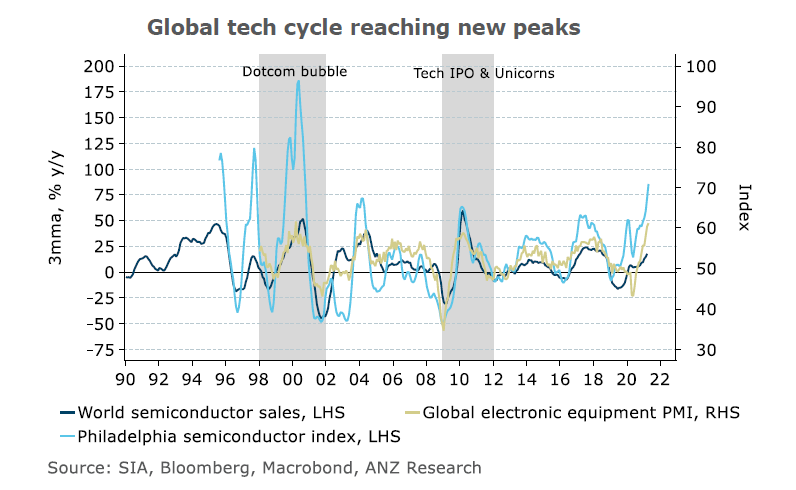

The global semiconductor market was worth $US440 billion in 2020, according to World Semiconductor Trade Statistics, after recording growth of 6.8 per cent, year on year. That’s forecast to accelerate to 12.5 per cent in 2021.

The global shift to work-from-home arrangements fuelled demand for personal computers throughout the pandemic. This coincided with an increase in companies investing in servers, computing and data storage infrastructure. In late 2020, the industry also began experiencing shortages due to bottlenecks in global supply chains.

In 2020, Taiwan’s export order demand rose 25.3 per cent year on year for electronic products and 13.6 per cent for infocomm products. Similarly, South Korea’s semiconductor exports have been rising at double-digit growth rates since mid-2020.

As such, the pandemic-driven demand boost will have a one-off impact. As vaccinations increase and economies reopen gradually, the proportion of the population required to telework will drop.

Supply

On the supply side, since late 2020, the semiconductor chip shortage that first affected the auto sector has spread to other industries. Manufacturers in the consumer electronics and home appliances segment are also facing a supply crunch which cause production delays.

According to the global electronic equipment’s suppliers’ delivery index, delivery times have increased to record levels. Reports suggest the wait for key components is three to six times longer than in the past.

As a result, tech-heavy economies such as Taiwan and South Korea face record-high production and export demand. Industry leaders believe the current semiconductor chip shortage will persist till 2022.

Shift

According to industry body GSMA, the use of 5G telecommunications tech will account for over 20 per cent of global connections by 2025, with particularly strong take-up across developed Asia, North America and Europe.

To support this shift, investments of nearly $US1.1 trillion will be required between 2020 and 2025, roughly 80 per cent of which will be in 5G networks. The capex plans of leading semiconductor companies are already at a decade high.

Impact

ANZ Research expects a sustained incremental boost to emerge from innovation and technological breakthroughs. The supply crunch will support the tech outlook until capacity expansion is able to meet demand.

The pandemic-driven demand, on the other hand, is a one-off disruptive factor and its incremental contribution to the current tech cycle upturn will be modest at best. Put together, ANZ Research believes these three factors will sustain the tech cycle momentum through 2021 and most of 2022. After that, it will increasingly hinge on innovation-driven demand.

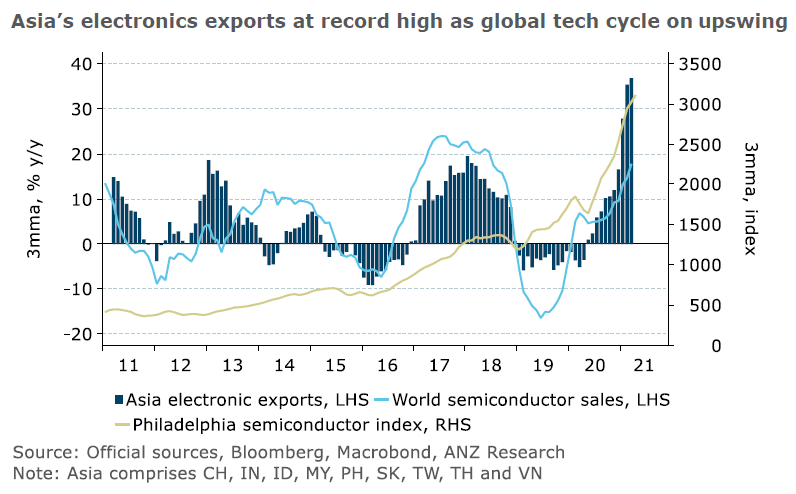

Strong exports were one of the key drivers of Asia’s recovery during the pandemic. Electronics exports became a game-changer for Asia’s tech economies.

At a time when demand for traditional goods declined, electronics-based exports saw historic growth rates. As a result, the share of electronics in Asia’s total exports rose to 33 per cent in the first quarter 2021, up from 29 per cent in 2018.

Going forward, ANZ Research expects the demand for tech exports will support and drive the region’s recovery through 2021 and most of 2022. After that, normalisation of the tech demand-supply balance will shift the focus to non-tech exports to catch up and even drive the region’s growth.

Bansi Madhavani is a Senior Economist at ANZ

This story is an edited version of an ANZ Research report. You can read the original report HERE.

Share

Related articles

-

Potential disinflationary effects would be balanced by a reduction in export competitiveness, ANZ Research suggests.

2026-04-01 00:00 -

Expert says businesses are responding to supply chain pressure with a focus on three elements — continuity, contingency, and liquidity.

2026-04-13 00:00 -

Data suggest momentum in underlying inflation is moderating, but RBA rise still expected in May, ANZ economist suggests.

2026-04-30 00:00

This publication is published by Australia and New Zealand Banking Group Limited ABN 11 005 357 522 (“ANZBGL”) in Australia. This publication is intended as thought-leadership material. It is not published with the intention of providing any direct or indirect recommendations relating to any financial product, asset class or trading strategy. The information in this publication is not intended to influence any person to make a decision in relation to a financial product or class of financial products. It is general in nature and does not take account of the circumstances of any individual or class of individuals. Nothing in this publication constitutes a recommendation, solicitation or offer by ANZBGL or its branches or subsidiaries (collectively “ANZ”) to you to acquire a product or service, or an offer by ANZ to provide you with other products or services. All information contained in this publication is based on information available at the time of publication. While this publication has been prepared in good faith, no representation, warranty, assurance or undertaking is or will be made, and no responsibility or liability is or will be accepted by ANZ in relation to the accuracy or completeness of this publication or the use of information contained in this publication. ANZ does not provide any financial, investment, legal or taxation advice in connection with this publication.