Published May 31, 2021

A sharp rise in core inflation across the United States and expectations of strong price pressure in coming months have raised concerns over a more-persistent inflation breakout.

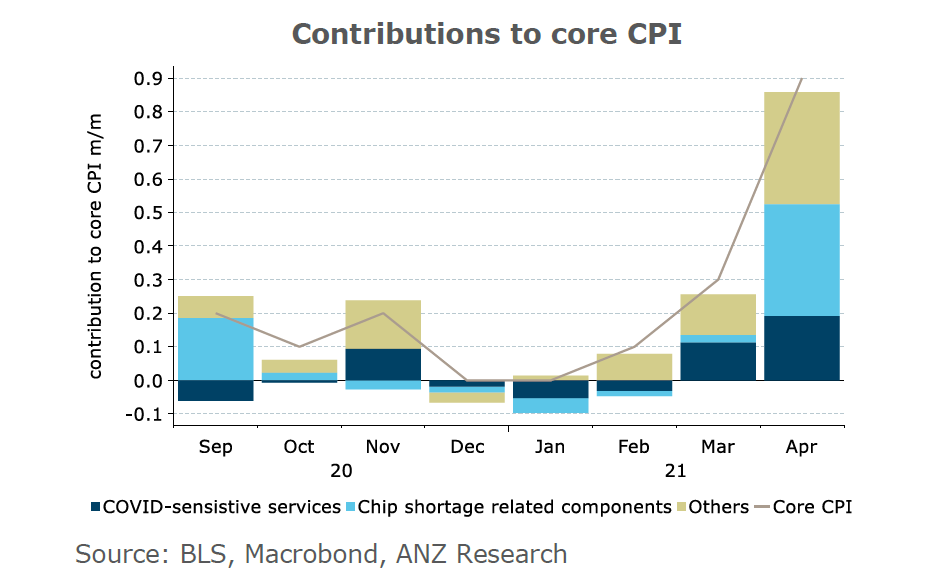

In April, the US Consumer Price Index (excluding fuel and energy) registered its largest month-on-month gain (0.9 per cent month on month) since the early 1980s.

The minutes of the latest US Federal Reserve meeting show, at least for now, most Fed members think inflation pressures are transitory. However, should inflation look to exceed the Fed’s 2 per cent mandate, members say the Fed won’t hesitate to act.

In coming months, inflation expectations and wages will determine whether inflation pressure becomes entrenched. As this evolves, the Fed will likely come under pressure to be more explicit about its tolerance for an inflation overshoot.

Volatile

US inflation is expected to remain volatile in the short term. A range of factors could intensify pricing pressure, including supply bottlenecks and pent-up spending on services as the economy reopens.

The US central bank is convinced it has time to be patient when setting policy and remains focused on returning the labour market to maximum employment.

Fed officials have shifted recent messaging in the face of criticism of a seemingly relaxed view to its price stability mandate. Specifically, there is a worry the Fed might let high inflation become embedded in expectations. To undo this, it would need to tighten aggressively, pushing the economy into recession. Although possible, this seems unlikely.

In recent decades, inflation-targeting central banks have tended to look at trends in core inflation as a guide to where overall consumer inflation is heading in the medium- to long-term. The latter is typically the objective or target of the central bank.

Although there are one or two headline measures of consumer prices, there are multiple measures of core inflation and no real consensus on which is best. Typically, a central bank will look at a suite of measures to assess underlying inflation trends.

For most advanced economies, over the last few decades, inflation tends to cycle around a stable long-term trend. The fluctuations depend on factors including imbalances between supply and demand, movement in import prices, and shocks.

Balance

Inflation expectations typically drive the long-term trend. The formation of the latter is important for forecasting inflation and for monetary policy, as the cycles around the trend tend to balance out over time.

Evidence suggests when central banks target a specific level of inflation, and have credibility in doing so, expectations tend to be anchored to that objective. The anchoring of inflation expectations helps to minimise the cyclical component around the trend.

Well-anchored inflation expectations have proven beneficial for the Fed, as they have enhanced its ability to pursue price stability and maximum employment mandates.

The Fed’s recent review of monetary policy seems to have recognised this benefit. Its employment mandate has moved from minimising deviations from full employment to eliminating shortfalls from maximum employment. This latter concept is a far broader and more inclusive employment mandate.

However, this anchoring of inflation expectations is not guaranteed given the substantive shock to the economy by the pandemic.

It is a stretch to conclude that the decades’ long structural drivers of low inflation – like technology, globalisation and inflation targeting – have suddenly flipped. And there are reasonable grounds to think the drivers of the current inflation spike – like supply bottlenecks, pent-up demand spending for services and expansionary fiscal policy – are temporary.

We cannot assume the broad structure of the economy will return to the way it was, once herd immunity has been achieved.

Indeed, the pandemic has given businesses time to consider their fundamentals, operations, and human and physical capital utilisation. This rethink may change the post-pandemic economic structure and how capital and labour are employed. The undercurrents presently driving inflation may not be transitory.

Participation

Workforce participation in the US is still being constrained by the pandemic. This may improve over coming months as vaccinations roll out. It’s also possible that some jobs that existed pre-pandemic are no longer needed, meaning the traditionally cited unemployment gap may not necessarily be a good indicator of slack in the labour market.

Wage pressure is likely if employers cannot find suitably qualified workers, especially in the face of solid demand. To this end, it will be worth watching a range of wage measures to gauge whether inflation is heading persistently higher.

This is in line with the messaging from key officials who have said they will be watching long-term inflation expectations to see if they remain consistent with the 2 per cent target. There is, however, no guidance from the Fed on how high inflation expectations need to get or for how long before they might adversely impact inflation, causing the central bank to react.

Most Fed members think current inflation pressures are transitory and should pass. That said, Fed members say they won’t hesitate to adjust policy if inflation expectations become inconsistent with its 2 per cent mandate.

ANZ Research is watching both wages and inflation expectations as potential triggers for a response from the Fed, but more clarity is needed from the central bank on its inflation tolerance.

Tom Kenny is a Senior Economist at ANZ

This story is an edited version of an ANZ Research report. You can read the original report HERE.