LIBOR Transition Customer Frequently Asked Questions

These updated Frequently Asked Questions (FAQ) should be read in conjunction with ANZ’s ‘LIBOR Transition Customer Presentation’ and the May 2020 version of the FAQs.

ANZ believes the information contained in these FAQs to be accurate as at April 2021. ANZ is not obliged to update the information or notify you should any information in these FAQs cease to be correct. The information contained in these FAQs is high level and intended to be a summary only. The FAQs should not be relied on as being current, complete or exhaustive. This information has not been prepared specifically for you or taking into account your particular circumstances.

LIBOR transition is a constantly evolving topic and this means information quickly becomes out of date. You should make sure to keep yourself up to date and informed on LIBOR Transition issues using current information.

The information in these FAQs is not intended in any way, and should not be interpreted, as ANZ providing advice to you. ANZ cannot advise you about LIBOR Transition and cannot provide you with any advice or recommendations. You must seek your own independent accounting, legal, regulatory, systems, tax or other advice about the impact of LIBOR Transition on your business.

These FAQs are intended for all customers with ANZ products referencing LIBOR. In case of conflict between these updated FAQs and the May 2020 version, the information in these updated FAQs take precedence.

To assist you, these updated FAQs include important information about recent market developments in, and ANZ’s current plan for LIBOR Transition.

The content of these FAQs have not been reviewed by any regulatory authority

The London Interbank Offered Rate (LIBOR) is known as the ‘most important number in the world’. It underpins about USD400 trillion worth of financial contracts globally, ranging from complex derivatives to home loans and credit cards. However, LIBOR is ending. The recent official announcement from the regulator of LIBOR’s administrator has started the countdown clock for the end of LIBOR in December 2021 (for non-USD LIBOR) and June 2023 (for USD LIBOR).

Industry working groups (supported by regulatory agencies) have set milestones for the transition away from LIBOR. Now is the time to take active steps to move away from LIBOR.

LIBOR Transition is a complex change to the financial markets and to lending arrangements. Planning ahead and actively engaging on these matters should enable customers to efficiently resolve their concerns.

The impact of LIBOR Transition will be different on each market participant. To assist in navigating these FAQs:

- If you have outstanding derivative transactions, consider in particular Derivatives

- If you have outstanding loan transactions, consider in particular Loans

- If you have outstanding trade and supply chain transactions, consider in particular Trade and supply chain finance

In any event, you should read the FAQs in their entirety.

LIBOR Transition introduces a new language to the financial market. We have included a Glossary of the more common terms used in the market in Glossary. The Glossary is not intended to be exhaustive but it does provide an introduction to the new language of risk-free rates.

Your usual ANZ representative is your point of contact for questions about transitioning your LIBOR referencing products from ANZ.

On 5 March 2021, the Financial Conduct Authority (FCA) announced all LIBOR settings will either cease to be published or will be considered no longer representative. The FCA is the regulator of the administrator of LIBOR (ICE Benchmark Administrator (IBA)).

The following LIBOR settings will permanently cease to be published on the cessation date set out in the table below.

Currency |

Setting |

Cessation Date |

|---|---|---|

|

All settings |

31 December 2021 |

|

All settings |

31 December 2021 |

|

Spot Next, 1W, 2M, 12M |

31 December 2021 |

|

Overnight, 1W, 2M, 12M |

31 December 2021 |

|

1W, 2M |

31 December 2021 |

|

Overnight, 12M |

30 June 2023 |

For the remaining LIBOR settings (1M, 3M and 6M in USD, GBP and JPY), the FCA announced these will no longer be considered representative of the underlying market and representativeness will not be restored from the dates set out below.

November 2021 Update

The FCA has announced that it will compel the continued publication of sterling and Japanese yen LIBOR settings for a limited time period after end-2021, using a 'synthetic' methodology (which as noted above, is not representative of the interbank funding market). This is currently proposed to only be permitted for use in certain legacy contracts and to be published only until the end of 2022 for JPY, with ongoing publication for GBP to be reviewed during 2022. As at the date of these FAQs, the FCA was still consulting on the specific contracts that will be entitled to use ‘synthetic’ LIBOR. More detail on this is set out below. For completeness, there is no current proposal from the FCA to compel the LIBOR administrator to publish EUR, CHF or USD LIBOR on a ‘synthetic’ basis.

Currency |

Setting |

Cessation Date |

JPY JPY |

1M, 3M, 6M |

31 December 2021 |

|---|---|---|

|

1M, 3M, 6M |

31 December 2021 |

|

1M, 3M, 6M |

30 June 2023 |

All 35 LIBOR settings will either cease to be published by the LIBOR administrator or no longer be representative immediately after the dates set out above. This means there will be a staggered cessation of LIBOR rates.

LIBOR is published in five currencies – USD, GBP, JPY, EUR and CHF. For each currency impacted by LIBOR cessation, national public authorities and private sector working groups have identified an alternative overnight risk-free rate (RFR) which can be used as an alternative benchmark for the existing interbank offered rate. These are intended to replace LIBOR for most financial instruments denominated in those currenciesdisclaimer. The identified RFR for each of the LIBOR currencies is set out in the table below:

Currency |

Setting |

|---|---|

|

SOFR (Secured Overnight Financing Rate) |

|

SONIA (Sterling Overnight Index Average) |

|

TONAR (Tokyo Overnight Average Rate) |

|

€STR (Euro Short Term Rate) |

|

SARON (Swiss Average Rate Overnight) |

Although the market is moving towards using RFRs in loans, derivatives and bonds, a RFR-based rate may not be appropriate for you in every circumstance. You may wish to consider alternative solutions and options that are more suitable to your specific objectives and needs. For example, you could consider a move to a fixed interest rate, or potentially an ANZ reference rate (or similar). ANZ is happy to discuss potential alternative rates with you.

ANZ expects most Trade & Supply Chain products to transition to Term RFRs rather than overnight RFRs due to the interest in advance/discounting nature of these products. Refer to Will ANZ be offering a Term RFR for loans? and the Trade and supply chain finance section for more detail.

The FCA announced it will consult in Q2 2021 on the continued publication on a ‘synthetic’ basis for certain GBP and JPY LIBOR settings. The proposed settings for ‘synthetic’ LIBOR are set out in the table below.

Currency |

Setting |

Synthetic LIBOR end date |

|---|---|---|

|

1M, 3M, 6M |

To be determined |

|

1M, 3M, 6M |

30 December 2022 |

The FCA has said it will continue to consider the case for requiring continued publication of US dollar 1M, 3M and 6M LIBOR settings on a ‘synthetic’ basis. No decision has been made yet for a synthetic USD LIBOR.

Publication of ‘synthetic’ rates is intended to protect consumer and market integrity, in particular in circumstances where it is unlikely to be feasible to convert certain legacy contracts to alternative reference rates (e.g. as described in Are any legislative solutions being considered?). Any ‘synthetic’ rates that are published would not necessarily be representative of underlying markets or economic reality. There is no guarantee the FCA will compel IBA to publish a ‘synthetic’ LIBOR rate beyond the official cessation dates or at all.

‘Synthetic’ LIBOR cannot be relied upon to transition legacy contracts.

November 2021 Update

The FCA has announced that it will compel the continued publication of sterling and Japanese yen LIBOR settings for a limited time period after end-2021, using a 'synthetic' methodology (which as noted above, is not representative).

What is Synthetic LIBOR?

The FCA has also confirmed that the methodology that will be used for ‘synthetic’ LIBOR is

- forward-looking term versions of the relevant risk-free rate (i.e. the ICE Term SONIA Reference Rates provided by ICE Benchmark Administration for sterling, and the Tokyo Term Risk Free Rates (TORF) provided by QUICK Benchmarks Inc., adjusted to be on a 360 day count basis, for Japanese yen), plus

- the respective ISDA fixed spread adjustment (that is published for the purpose of ISDA’s IBOR Fallbacks for the 6 LIBOR settings) – see Did the FCA announcement fix ISDA’s spread adjustment?: below for further details.

How long will Synthetic LIBOR be published for?

The current position is that ‘synthetic’ LIBOR will only be published until the end of 2022 in the case of JPY LIBOR, and ongoing use of the power to compel IBA to continue publication of GBP LIBOR will be reviewed by the FCA during 2022.

Which contracts are eligible to use Synthetic LIBOR?

Synthetic LIBOR is permitted for use in legacy contracts other than cleared derivatives, that have not been changed at or ahead of 31 December 2021. The use of Synthetic LIBOR is not permitted in any new contracts.

ANZ will not support the use of Synthetic LIBOR in any new contracts.

What about other currencies?

There is no current proposal to publish EUR, CHF or USD LIBOR on a "synthetic" basis.

The benchmark rates for the currencies of Singapore, Thailand, India and the Philippines need to be replaced due to their dependency on USD LIBOR as an input. The scheduled cessation of USD LIBOR will materially impact the operation of these rates.

Each of the fallbacks for these Asian IBOR benchmark rates use ‘Adjusted SOFR’ compounded in arrears for the relevant setting (as published by BISL) together with a credit adjustment spread instead of USD LIBOR. The Asian IBOR benchmark fallback rates can only be used for legacy transactions/contracts as prescribed by the local authority. You can find more information about timing of the use of rates in different markets in When will LIBOR stop being used in new product issuances? Bloomberg will not be publishing Fallback SOR or Fallback THBFIX. These rates will be provided by ABS Administration Co Pte. Ltd. and the Bank of Thailand respectively.

Figure 1

Currency |

Asian IBOR Benchmark |

Authority |

Asian IBOR Benchmark Fallback |

Asian Replacement Rate |

|---|---|---|---|---|

|

SOR |

Monetary Authority of Singapore |

Singapore Overnight Rate Average (SORA) |

|

|

THBFIX |

Bank of Thailand |

Thai Overnight RepurchaseRate (THOR) |

|

|

MIFOR |

Reserve Bank of India |

||

|

PHIREF |

Banker’s Associationof Philippines |

PHIREF using compoundedSOFR Adjusted – set in arrears |

Still in development |

The fallback and replacement rate for each of these Asian IBOR benchmarks are set out in Fig.1 above.

ANZ’s current understanding is that existing transactions referencing these Asian IBOR benchmarks can continue to do so until 30 June 2023. After 30 June 2023, their respective replacement rates will need to be used. This is subject to future guidance from the regulators or the applicable administrators for the continued use and construction of these benchmarks.

Although LIBOR rates are ceasing at the end of December 2021 (for non-USD) and June 2023 (for USD), their use in new product issuance must stop before then. Through the national working groups in each country (firmly supported by relevant regulatory agencies), recommended milestones have been published to inform market participants of when they should be ceasing new issuance of products referencing LIBOR. These milestone dates are different depending on the benchmark rate and product type. Fig.2 below provides a summary of these milestones. This table is current as at end of March 2021.

The milestones are subject to change and may also change without notice.

Figure 2. Summary of milestones

Milestone Date and CCY |

Source |

Product & Action |

|---|---|---|

31 March 2021 |

UK RFRWG |

Cease issuance of new GBP LIBOR bonds, loans, securitisations and linear derivatives expiring after end-2021, except forrisk management of positions |

30 April 2021 |

SC-STS |

All lenders to offer SORA products and stop usage of SOR in new cash market products that mature after end-2021 |

30 June 2021 |

ARRC |

Cessation of use of USD LIBOR in new bi-lateral business loans, securitizations and derivativesdisclaimer |

30 June 2021 |

UK RFRWG |

Cease issuance of new GBP LIBOR non-linear derivatives except for risk management of positions |

30 June 2021 |

CIC on JPY |

Cease the issuance of new loans and bonds referencing LIBOR |

1 July 2021 |

BOT |

Financial institutions are prohibited to offer new loans, bonds, structured products and other securities referencing THBFIX maturing after 30 June 2023 |

31 July 2021 |

Term rate sub-groupof CIC on JPY |

New quoting conventions for JPY interest rate swaps market to be based on TONA |

Q2/Q3 2021 |

UK RFRWG |

Cease initiation of new cross-currency derivatives with a GBP LIBOR-linked leg |

30 September 2021 |

ARRC |

Cessation of use of USD LIBOR in new collateralised loan obligations |

30 September 2021 |

SC-STS |

Cease use of SOR in new derivatives All banks to stop new use of SIBOR |

30 September 2021 |

Term rate sub-groupof CIC on JPY |

No new JPY LIBOR interest rate swaps except for risk management of existing positions |

31 December 2021 |

FCA |

GBP, EUR, JPY, CHF LIBOR all tenors end |

31 December 2021 |

FCA |

1W and 2M USD LIBOR end |

31 December 2021 |

US Fed, FDIC, OCC |

Cease entering into new contracts using USD LIBOR as soon as practical and in any event by December 2021, except forlimited circumstancesdisclaimer |

31 December 2021 |

HKMA |

Authorised institutions should cease to issue new LIBOR based products that mature after 2021 |

31 March 2022 |

SC-STS |

6M SIBOR ends |

31 December 2022 |

SC-STS |

Aim to complete active transition for legacy SOR cash contracts |

30 June 2023 |

FCA |

O/N, 1M, 3M, 6M & 12M USD LIBOR end |

30 June 2023 |

SC-STS |

SOR ends |

31 December 2024 |

SC-STS |

1M & 3M SIBOR end |

31 December 2024 |

JBATA |

JPY Euroyen TIBOR end (subject to outcome of industry consultation) |

UK RFRWG – Working Group on Sterling Risk-Free Reference Rates

SC-STS – Steering Committee for SOR and SIBOR Transition to SORA

ARRC – Alternative Reference Rates Committee

CIC on JPY – Cross-Industry Committee on Japanese Yen Interest Rate Benchmarks

HKMA – Hong Kong Monetary Authority

BOT – Bank of Thailand

FCA – Financial Conduct Authority

US Fed – Board of Governors of the Federal Reserve System

FDIC – Federal Deposit Insurance Corporation

OCC – Office of the Comptroller of the Currency

JBATA – Japan Banker’s Association TIBOR Administration

Yes. For T&SC products ANZ is able to offer Term RFR products in most instances. As set out below, there are Term RFR Rates currently available for three currencies: GBP (Term SONIA); USD (Term SOFR); and JPY (TORF). For euro, T&SC will be using Euribor.

One point to highlight is that Term RFRs will not be published for all the same tenors as LIBOR is currently (the table below sets out the tenors for which the respective Term RFR will be published). In particular, Term RFRs will not be published for 1 week or 2 month tenors, and in the case of TORF it will not be published for the 12 month tenor either. ANZ’s standard position will for any drawings for non-standard periods will be to use the next available rate. For TORF, as there is no twelve month rate any drawings requests for JPY for transactions any drawing requested for greater than 6 months will be priced by way of our cost of funds rate.

RFR Source Rates

For drawings denominated in: |

The Term RFR is |

|

|---|---|---|

|

Term SOFR |

ARRC announced it has selected CME Group as the administrator for a forwarnd-looking SOFR term rate CME Term SOFR Reference Rates are derived from CME SOFR Futures and published for 1-month, 3-month, 6-month and 12-month tenors |

|

Term SONIA |

ANZ will be using Term SONIA published by Refinitiv. Refinitiv Term SONIA Reference Rates are derived from SONIA OIS contracts and published for 1-month, 3-month, 6-month and 12-month tenors. Term SONIA is published every London business day at 11.50am London time |

|

TORF |

Tokyo Term Risk Free rates are derived from JPY TONA OIS contracts and published for 1-month, 3-month, 6-month tenors. TORF is published every Tokyo business day around 17.00 JST |

|

Euribor |

Although not a term RFR, ANZ intends to use Euribor as the replacement rate for EUR drawings |

RFRs are published on a daily basis. Product terms should give parties sufficient time for notice and collection of payment. To calculate an interest amount based on a RFR for a particular interest period, 4 interest calculation methods currently exist. The 4 interest calculation methods are:

- Observation period shift

- Lookback

- Payment delay

- Lockout

Each of the 4 interest calculation methods are described in more detail in the diagrams below. These methods can be applied to loans, derivatives and bonds. Note that payment delay is not typically used in loans.

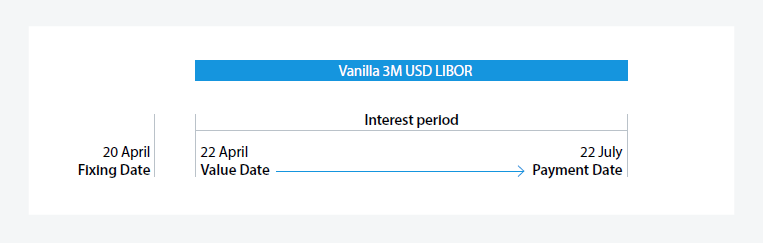

3M LIBOR Interest period

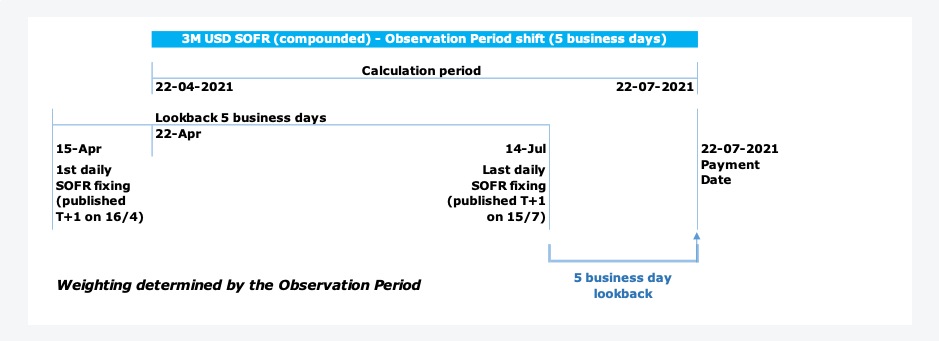

Observation period shift example

Observation period shift – keeps existing LIBOR payment dates

• 5 business day observation period shift where the start and end date of the calculation period are moved to the dates 5 business days earlier

• SOFR is observed each day SOFR is published in the observation period

• In the calculation of the daily compounded interest amount, there are 2 inputs – (i) the observed SOFR and (ii) the weighting of each day. For an observation shift, the weighting for each day is determined by the relevant day in the observation period

• Each business day in a week is given a weighting of ‘1’ except for Friday which has a weighting of ‘3’ (as Friday covers 3 calendar days). If there is a bank holiday in the week then the day prior is given a weighting of ‘2’ (representing the business day and the next day)

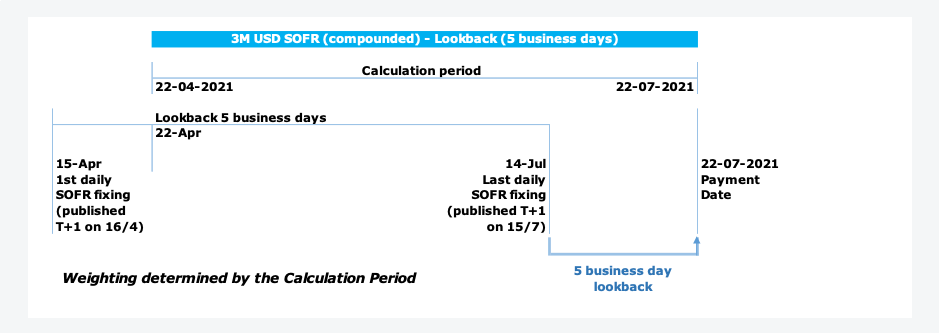

Lookback example

Lookback – keeps existing LIBOR payment dates

- SOFR is observed on each day of the calculation period using the SOFR rate published 5 business days earlier

- Weighting for each day is determined by the relevant day in the calculation period

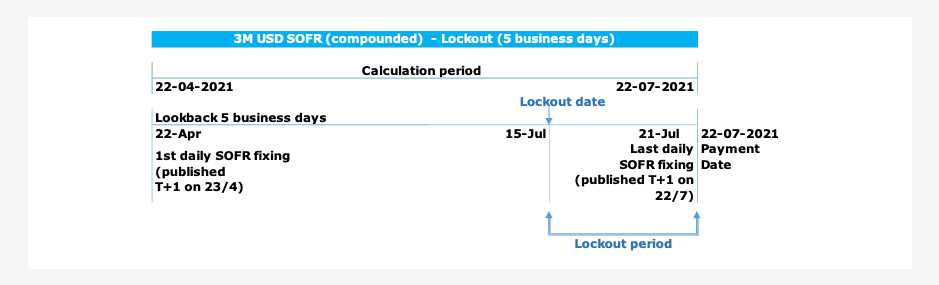

Lockout example

Lockout – keeps the existing LIBOR payment dates and aligns SOFR fixings with the original LIBOR interest period but with a lockout period

- SOFR is observed on each day of the period aligned to the original LIBOR interest period

- SOFR for each day in the lockout period. This means SOFR is then fixed observed on the 1st day of the lockout period

(i.e. the lockout date) will be used for each of the remaining business days in the lockout period. This allows for the final interest amount to be known 4 business days before the payment date

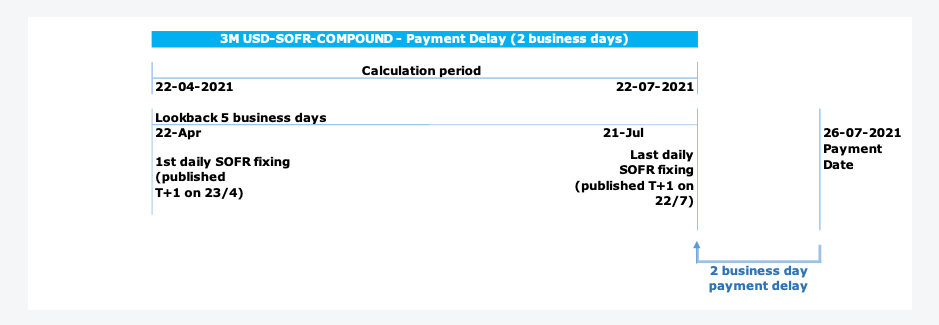

Payment Delay example

Payment delay – aligns SOFR fixings with the original LIBOR interest period (for swaps market)

- SOFR is observed on each day of the original LIBOR interest period. This requires the use of a 2 business day payment delayon both legs of the swap

- This is similar to the convention used in ISDA’s USD-SOFR-COMPOUND floating rate option which uses a 2 business day offset

This communication is made by Australia and New Zealand Banking Group Limited (ABN 11 005 357 522) in Australia and outside Australia by either its branches or subsidiaries (each is referred to in this important notice as ‘ANZ’). It is intended for ANZ’s institutional, professional or wholesale customers, and not for individuals or retail persons. It should not be forwarded, copied or distributed. The information in this communication is general in nature, and does not constitute personal financial product advice or take into account your objectives, financial situation or needs. This communication does not constitute an offer of financial accommodation.

This communication:

- does not constitute advice and ANZ does not expect you to rely on it. ANZ does not provide any financial, investment, legal or taxation advice in connection with this communication;

- is not a recommendation and is not intended to influence you or any other person to make a decision; and

- is not an invitation, solicitation or offer by ANZ to you to acquire a product or service, or an offer by ANZ to provide you with other products or services.

The information in this communication was prepared by ANZ in good faith from publicly available sources and while care has been taken in compiling it:

- ANZ has not independently verified the content of the underlying information;

- the information is high level, intended as a summary only and should not be relied on as being current, complete or exhaustive;

- ANZ does not undertake to update the information in this communication or notify you should any information contained in this communication cease to be current or correct; and

- no representation, warranty, assurance or undertaking, is or will be made, and no responsibility or liability is or will be accepted by ANZ in relation to its currency, accuracy or completeness.

ANZ, and its directors, officers and employees, expressly disclaim any responsibility and shall not be liable for any loss, damage, claim, liability, proceedings, cost or expense arising directly or indirectly and whether in tort (including negligence), contract, equity or otherwise out of or in connection with the contents of and/or any omissions from this communication to the extent permissible under relevant law.

LIBOR Transition is a constantly evolving topic, and this means information quickly becomes out of date. Make sure you keep yourself up to date and informed on transition issues using current information.

If this communication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted or contain viruses. ANZ does not accept liability for any damage caused as a result of electronic transmission of this communication.

The content of this communication has not been reviewed by any regulatory authority. ‘ANZ’, ANZ’s logo and ANZ’s colour blue are trademarks of ANZ.

ANZ is aware that there are other rates in development that may also fill part of the role previously played by LIBOR (for example AMERIBOR). ANZ’s current view is that it does not see a use case for these alternative rates. However, ANZ continues to monitor market developments.

ReturnIndustry consultation on the methodology for Modified MIFOR is taking place. Modified MIFOR is for use in new transactions/contracts on cessation of LIBOR

Return