A recent surge in food inflation in India poses a key challenge for the country’s central bank, which is already facing headline inflation above its upper target band.

The Reserve Bank of India (RBI) now has the difficult task of achieving its 4 per cent inflation mandate while curbing any potential generalisation of price pressures due to elevated food costs. How should it respond?

The RBI rightly dialled up its hawkishness at its August meeting and is likely to keep a tight leash on liquidity in response to this latest challenge. Without the right kind of public policy intervention, or if the monsoon rainfall deficit widens markedly, another rate hike in October or December can’t be ruled out.

As food prices continue to rise, a study by ANZ Research shows the food inflation cannot be shrugged off as entirely transient.

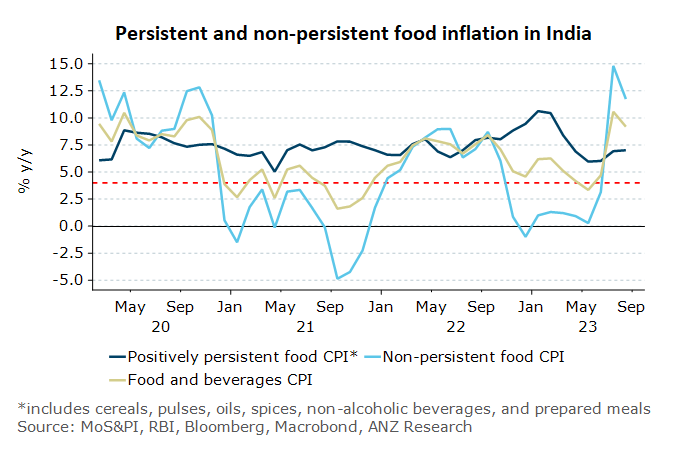

Food consumer price indices (CPIs) for cereals, pulses, oilseeds, non-alcoholic beverages, spices and prepared meals show positive persistence of price shocks, meaning a shock in their prices tends to linger for the next twelve months. These items occupy 28 per cent of the CPI basket collectively, more than 60 per cent of the food-and-beverages subindex.

While the combined inflation in these six items is high and discomforting, it is not a recent problem. Persistent food inflation has been rising since 2018, after falling between late 2015 and 2017.

By late 2019, it was already trending above 4 per cent, averaging 7.4 per cent since the beginning of the pandemic. It hit 10 per cent at the start of 2023 and then moderated to 6 per cent by May, before picking up again in June and climbing up to 7 per cent in July.

Vegetables and fruits, by contrast, exhibit negative persistence of inflation. This means their price shocks reverse over twelve months, making episodic high or low inflation temporary.

The effects of price shocks on food items with a shorter cropping cycle is short lived. Potato, onion and tomato, for instance, have average cropping cycles of 80 to 100 days. A sharp rise in vegetable prices can quickly stimulate more supply. The average national tomato price, for instance, has already fallen to 40 rupees a kilogram from its peak of 140 in July.

Amid episodes of elevated persistent food inflation, it is only sharp declines in the prices of volatile items like vegetables that caused overall food inflation to fall occasionally to (or below) 4 per cent in recent years. Relying on volatile items to bring food inflation down durably is akin to banking on luck.

Second round

What can the RBI do? Food prices do not fall within the ambit of monetary policy directly. But insofar as they impact household inflation expectations, they can feed into the prices of a broader set of goods and services, creating ‘second-round’ effects.

ANZ Research has found the historical variation in inflation expectations of Indian households can be explained mostly by food inflation and the ‘stickiness’ of inflation expectations.

Within food inflation, it is inflation in the ‘persistent’ categories that most closely tracks the changes in expectations. ANZ Research thinks households won’t be strongly influenced by the recent vegetable price shocks in forming inflation expectations. But they may respond to high inflation in persistent food categories, notably cereals, pulses, spices and prepared meals.

What might that response look like? In theory, second-round effects mean households faced with high current inflation expect higher future inflation, stoking wages, aggregate demand and prices. Such wage-price spirals are scary but exist more in theory than reality.

For India, ANZ Research found core inflation rises only minimally over twelve months in response to high headline inflation. In other words, second-round effects are there, but weak.

This is partly because India’s labour market is dominated by the informal sector, where workers are typically low skilled and have little bargaining power. However, for an RBI focused on bringing inflation down, even the slightest rise in core inflation due to second-round effects may not be palatable.

Public policy is certainly the more effective lever to bring persistent food inflation down. The export ban on rice echoes this sentiment, but more measures will be needed.

India may be headed for its lowest rainfall in eight years, and the area sown with key kharif crops, like pulses, is quite low compared to last year. This does not augur well for inflation, especially with oil prices, an old adversary, making a bullish comeback.

Dhiraj Nim is an Economist at ANZ Research