India’s growth has captured the attention of the world. But the right kind of reform, targeting fundamental drivers including labour, capital and productivity, could help accelerate that growth - and keep it higher for longer.

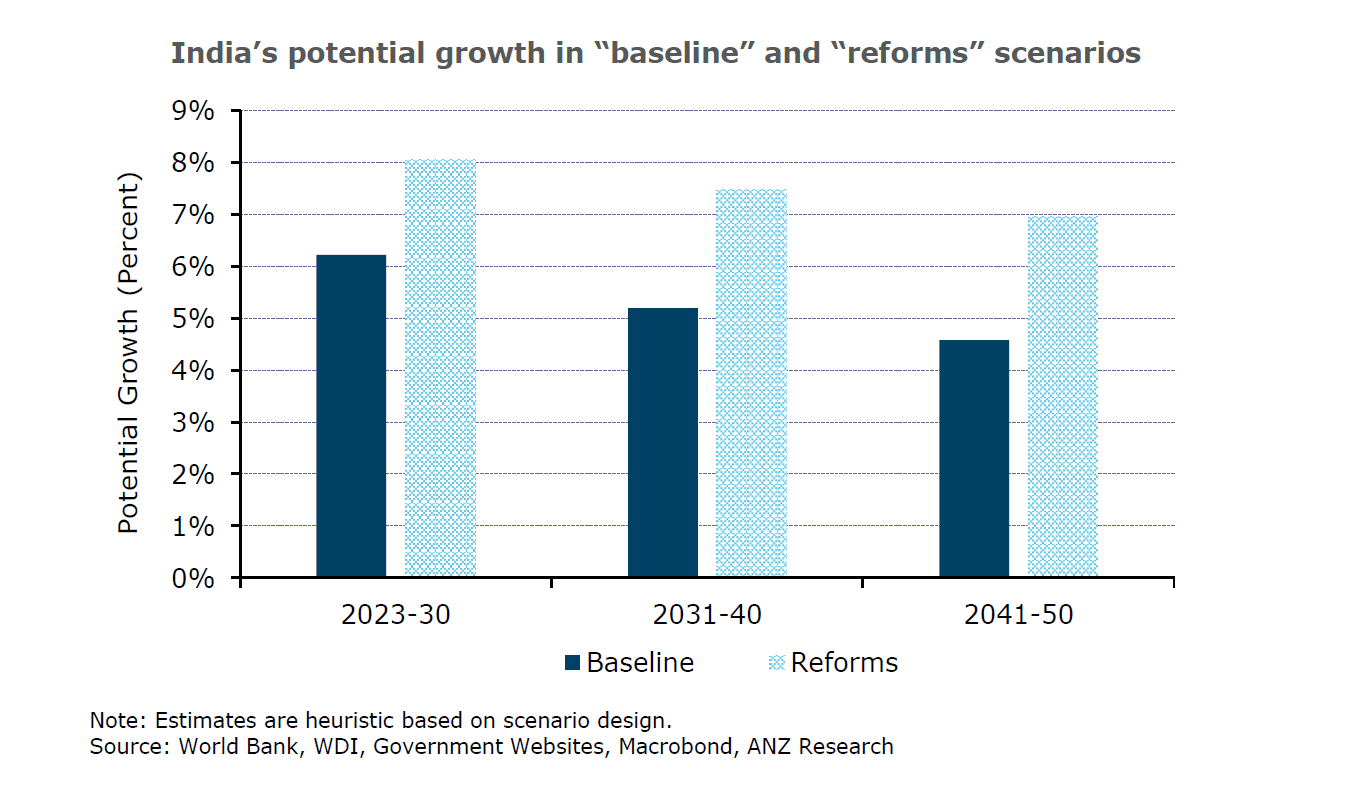

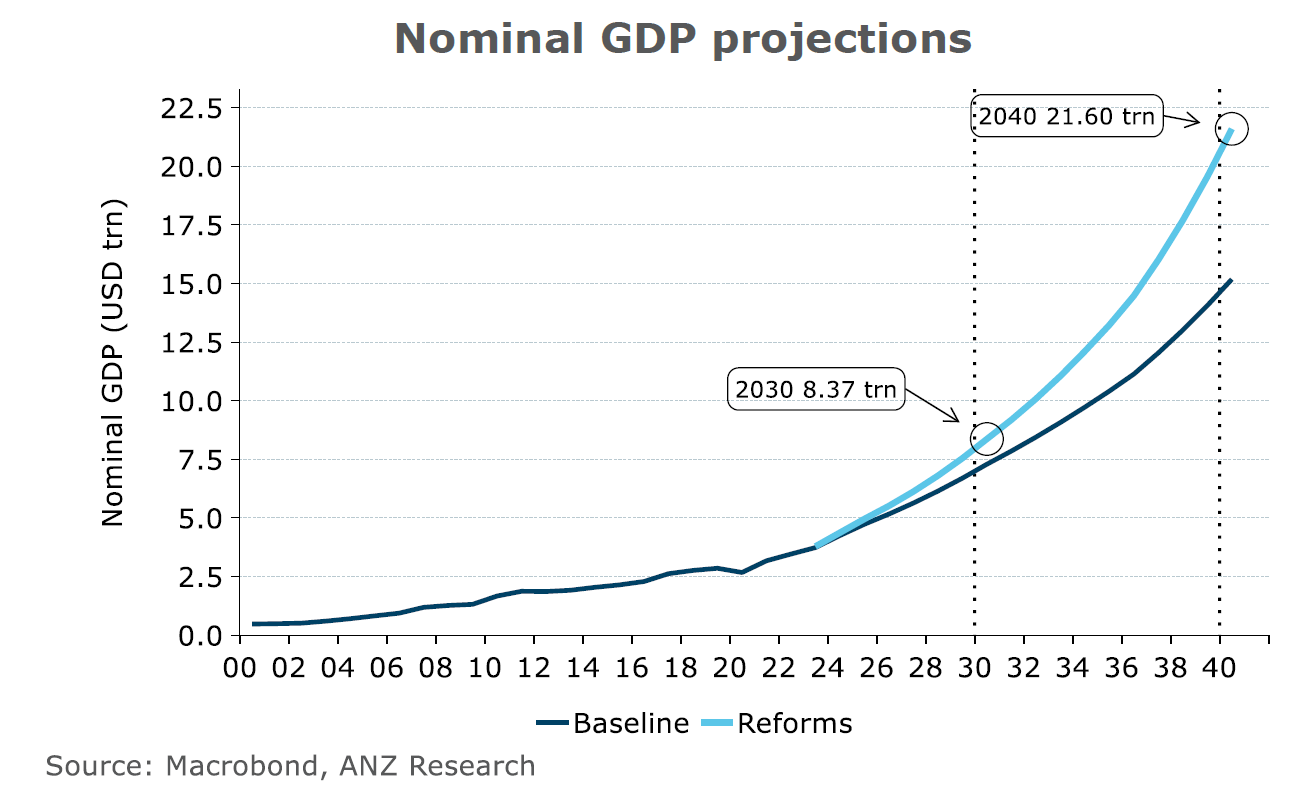

A growth-accounting exercise by ANZ Research shows India has a chance to lift its average gross domestic product (GDP) growth to 8 per cent through 2030. In such a scenario, growth could potentially remain above 7 per cent for some time, while nominal GDP could surpass $US20 trillion by 2040. Per capita income, a measure of economic prosperity, could also rise to $US13,000 by 2040. This is just below the current threshold for a high-income country.

Conversely, if India’s reform momentum is lacklustre, a less exciting picture is on the cards. Average potential growth could peak at 6.2 per cent this decade and then slow to 4.6 per cent by 2050. Living standards, in such a scenario, will also tread a very ordinary path, reaching $US9500 by 2040. Nominal GDP could also remain below $US15 trillion by the end of next decade.

The stark difference between these two possibilities is the pace of reform to lift drivers of growth. Importantly, the more optimistic reform scenario assumes India’s labour force participation rate (LFPR) rises to 60 per cent and mean schooling years among adults lifts by 12 years by 2050.

India’s LFPR has been falling according to World Bank data. At 53 per cent, it is now far below the rest of Asia’s 70 per cent average, and lower than India’s own historical best 60 per cent. Depressed workforce participation among women due to complex socio-economic factors has been a constraint.

Mean schooling years among Indian adults is currently 6.7 years, the lowest among major Asian economies. It has risen by a meagre 0.1 years annually in the recent past.

India will need ambition here. It is fast approaching a point when its age-dependency ratio - a country’s share of working age-to-dependent population - will bottom out in the early 2030s. The lower this ratio, the better the prospects of economic growth.

Reaching a target of 12 mean schooling years will help offset some of the drag from oncoming unfavourable demographic shifts. Only Malaysia and Korea have managed this feat so far in the Asian cohort. The effort needed is substantial.

Unfinished

There are other unfinished chapters in India’s story which will need intervention. Surplus labour needs to be shifted away from agriculture to industry, while agricultural productivity and wages need to rise.

Roughly half of the workforce is engaged in agriculture. Data show even agricultural workers who leave are mostly absorbed by other less-productive sectors like construction. Skilling and upskilling the workforce will be imperative. Capital investments in agriculture need to rise to ensure higher wages and productivity.

Informality must be reduced, easing constraints on firm-level productivity and innovation. Average firm size in the informal sector is below five workers, constraining economies of scale. Technology adoption is also deeply divided. Only 40 per cent of firms with less than 10 workers use the internet, as opposed to 100 per cent of large firms.

These challenges look formidable, but timely policy intervention in recent years has helped set the ball rolling toward a solution. These initiatives do not remove the need for deeper reform but will ensure India’s economic future is better than the lacklustre scenario described above.

The flagship Make in India campaign and an improving export ecosystem are ramping up manufacturing. Global producers hunting for alternatives to China are viewing India in a brighter light. The latter’s rapidly rising production and exports of mobile phones are a case in point.

The Indian government’s massive push to infrastructure and digitisation will ensure capital formation picks up pace and productivity growth is sustained. Robust contributions from capital and productivity have been vital to economic growth in the last two decades.

India’s investment in its digital infrastructure is especially promising. Tools like unique digital identity, an enviable digital payments interface, and seamless data exchange between platforms, will all help plug fiscal spending leakages, enhance financial inclusion, widen the reach of businesses and customers, and foster education and skilling. These are only some of the many benefits of the rapid technological strides India is taking.

Undeniable

India will become an important engine of global growth – that is undeniable. But whether it can realise its own economic potential depends on how quickly and aggressively it can untangle its deep-rooted problems.

The foundation for growth that capitalises on India’s demographic dividend is not yet in place. A high rate of growth is not sufficient for inclusive growth. What is certain, however, is India’s economic future will not be unexciting.

Sanjay Mathur is Chief Economist, Southeast Asia and India, Dhiraj Nim is Economist/FX Strategist, and Arindam Chakraborty is an Economist at ANZ

This is an edited excerpt from the ANZ Research report “India: the potential for faster growth”, published July 20, 2023