-

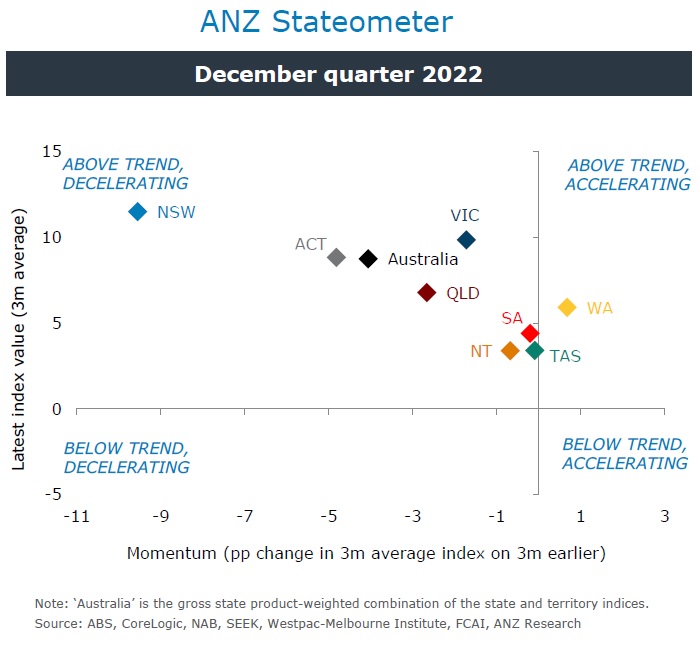

Economic momentum across Australia’s states and territories remained above trend in the final quarter of calendar 2022, the ANZ Stateometer found, but the peak appears behind us.

Parts of the Australian economy are beginning to slow down but overall the country remains resilient. The housing and business sectors are past their best, while consumption is holding up despite pockets of weakness.

The labour market is proving to be exceptionally healthy, while resource-driven trade demand is holding up well given the global slowdown.

According to the ANZ Stateometer, economic momentum decelerated through the December quarter, but stayed above trend in all states and territories except Western Australia.

Speed bumps in the form of further interest rate hikes are likely to slow economic performance in the coming months.

ANZ Research still does not see a recession, thanks to the strong starting point for household and business finances before the tightening cycle began, and the relative resilience of economic activity.

video

Base effect

Earlier in February, ANZ Research upwardly revised its forecast for the Reserve Bank of Australia’s target cash rate to 4.1 per cent by May 2023, given the persistence of inflationary pressure.

The road to getting inflation back to the target band means the RBA is unlikely to cut rates in a hurry. The cash rate could stay at 4.1 per cent until late 2024.

Most of the deceleration seen in New South Wales, Victoria and Queensland was caused by a material decline in the consumer component. There is a base effect at play here, given many states were coming out of COVID-19 delta-variant-wave lockdowns in late 2021.

High frequency indicators, such as ANZ-observed spending, suggest there is still appetite for discretionary consumption nationally.

The labour component remains above trend, especially across NSW, Victoria and the Australian Capital Territory, reflecting tight conditions. Business is a mixed picture, with NSW and Victoria holding up relatively well, while Queensland and WA slowed.

Trade boosted the overall economic performance. An increase in overseas arrivals supported NSW, Victoria and the ACT, while strong resource exports were positive for Queensland, WA and the Northern Territory.

Trend

Across the key states, the ANZ Stateometer showed a decline in NSW’s economic performance in the December quarter, after a rapid rise in the three months to September.

Victoria’s economic performance pulled back slightly but remains above trend. In Queensland, the economic performance softened, with the housing and business components detracting from the overall index.

The ANZ Stateometer is a set of composite indices that measure economic performance across Australia’s states and territories.

For each jurisdiction, the index extracts the common trend across multiple indicators (between 24 and 32, depending on data available in the jurisdiction). The economic indicators are monthly data series and cover the consumer, business, housing, labour and trade sectors.

Developments across this diverse country are rarely uniform and we hope these geographically specific indices help you to see through the haze of state by state data and more intuitively piece together the state of the national economy.

Bansi Madhavani, & Adelaide Timbrell are Senior Economists, Madeline Dunk is an Economist and Arindam Chakraborty is a Junior Economist at ANZ

This story is an edited excerpt from the ANZ Stateometer, published February 23, 2023

Share

|

Receive insights direct to your inbox |

Related articles

-

Two ANZ experts chat through the outlook for bond and loan markets ahead of the 2023 ANZ Debt Conference.

2023-02-19 00:00 -

Any potential slowdown in Asia outside China is likely to be a garden-variety one.

2023-02-07 05:30 -

Capital allocation will be a critical consideration for businesses in 2023.

2023-01-17 05:30

This publication is published by Australia and New Zealand Banking Group Limited ABN 11 005 357 522 (“ANZBGL”) in Australia. This publication is intended as thought-leadership material. It is not published with the intention of providing any direct or indirect recommendations relating to any financial product, asset class or trading strategy. The information in this publication is not intended to influence any person to make a decision in relation to a financial product or class of financial products. It is general in nature and does not take account of the circumstances of any individual or class of individuals. Nothing in this publication constitutes a recommendation, solicitation or offer by ANZBGL or its branches or subsidiaries (collectively “ANZ”) to you to acquire a product or service, or an offer by ANZ to provide you with other products or services. All information contained in this publication is based on information available at the time of publication. While this publication has been prepared in good faith, no representation, warranty, assurance or undertaking is or will be made, and no responsibility or liability is or will be accepted by ANZ in relation to the accuracy or completeness of this publication or the use of information contained in this publication. ANZ does not provide any financial, investment, legal or taxation advice in connection with this publication.