-

Published May 11, 2021

This is very different Australian Federal Budget to what many expected. The Australian government has announced new spending worth $A95.9 billion over the five years from 2020-21 - which is almost enough to offset the improvement in the fiscal position of $A104.3 billion from the stronger economy.

This level of spending, despite the strong economic recovery, was a surprise to ANZ Research and shows a strong commitment to a new fiscal strategy of continuing to spend until the unemployment rate is below where it was prior to the pandemic.

The level of spending creates upside risk to the growth outlook, which is intentional. But it also increases the risk of overheating down the track. It will do little to dissuade the market from thinking Reserve Bank of Australia rate hikes will come sooner than 2024.

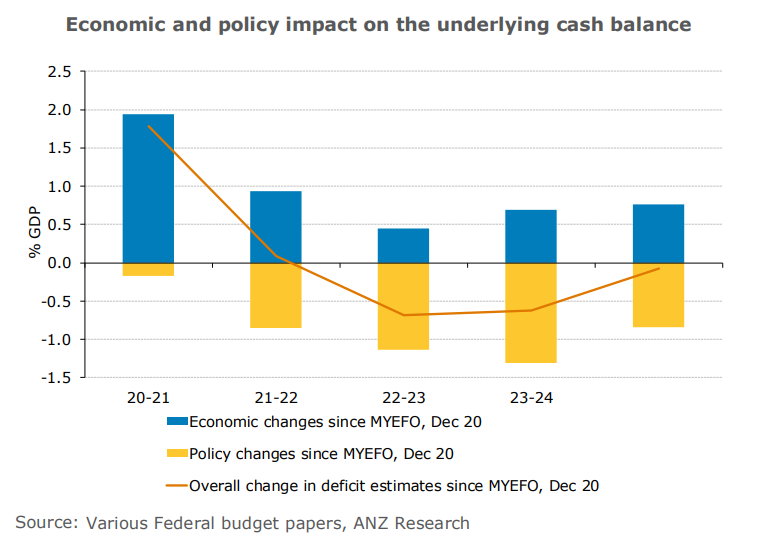

As a consequence of the additional spending, the improvement in the fiscal deficit is much less than expected. The underlying cash balance for 2020-21 is expected to be a deficit of $A161 billion (a fall of 7.8 per cent of GDP).

From there the underlying cash deficit improves to $A106.6 billion in 2021-22 (a decline 5 per cent of GDP) and continues to improve with the deficit narrowing to $A57 billion (2.4 per cent of GDP) by 2024-25.

Relative to the 2020-21 mid-year economic and fiscal outlook (MYEFO), this is an improvement of just $A7.9 billion over the forward estimates. From 2022-23 onwards, the deficit is actually forecast to be larger in each year than at MYEFO.

Foot on the pedal

The better economic outcomes in 2020-21 mean Australia’s payments-to-GDP ratio is forecast to peak at 32 per cent of GDP, down from 33.5 per cent at MYEFO. However, the boost in spending means beyond this the ratio is largely unchanged. Given the much better economic outlook, this level of spending represents a very expansionary fiscal setting.

Receipts, on the other hand, are up around $A82 billion compared with MYEFO, yet as a share of GDP they are lower than at MYEFO. ANZ Research thinks the tax forecasts are very cautious and there is upside risk going forward. It wouldn’t shock to see smaller-than-forecast deficits at MYEFO.

The economic forecasts underpinning the budget appear quite reasonable. For 2021-22, the government expects real GDP to grow by 1.25 per cent, broadly in line with ANZ Research and the RBA’s estimates.

For nominal GDP - the key parameter for the deficit - the government’s forecasts are generally conservative. For the 2020-21 year, the numbers are broadly in line with ANZ Research (3.75 per cent vs 3.5 per cent), although they are a considerably lower in 2021-22 (at 3.5 per cent vs 6.4 per cent), with the underlying expectation the terms of trade fall a sharp 8 per cent. A further forecast decline in 2022-23 is expected to weigh on nominal GDP.

Treasury has significantly upgraded its labour market forecasts since MYEFO in December. The unemployment rate is forecast to fall to 5.5 per cent in the second quarter, almost 2 percentage points lower than the 7.25 per cent forecast at MYEFO.

Employment growth is then forecast at 1 per cent, year on year, through 2021-22 and 2022-23. ANZ Research is more optimistic, forecasting 2.5 per cent year-on-year employment growth in mid-2022.

Despite the uneven recovery, Treasury expects employment growth of 1 per cent year-on-year will be enough to bring the unemployment rate down to 5 per cent by June 2022 and 4.75 per cent by June 2023.

This will be helped by slow labour force growth, largely due to closed borders restricting population growth, but also due to assumptions of a flat participation rate.

ANZ Research is again more optimistic, forecasting an unemployment rate of 4.8 per cent by end-2021 and 4.4 per cent by end-2022, even with expectations of rising participation over that period.

Gradual

Despite the significant upgrade to the labour market outlook, Treasury is forecasting only a very gradual pick-up in wages growth. The wage price index is only expected to rise 1.5 per cent year on year by mid-2022 and 2.25 per cent year on year by mid-2023. It is not forecast to get above the RBA’s target of 3 per cent before mid-decade at least.

Taken together with the CPI inflation forecasts, this also means the government expects flat to falling real wages at least until 2024-25.

The government has noted upside risk to the wages growth outlook in the form of stronger labour market conditions and ongoing international border closures exacerbating labour shortages in some industries, putting upward pressure on wage growth. ANZ Research thinks this upside risk will very likely materialise.

Capital spending for 2020-21 through to 2023-24 is almost unchanged on the 2020 budget, though as a share of GDP it is lower in the earlier years. Though mostly unchanged at the headline level, compositionally there has been some change.

With the deficit only slightly better, net debt is forecast to continue rising quite rapidly over the forecast horizon. However, as a share of GDP it is lower than previous estimates given the rise in GDP. Still, net debt as a share of GDP is projected to rise from 30 per cent in 2020-21 to 40.9 per cent in 2024-25 – an all-time high.

David Plank is Head of Australian Economics, Felicity Emmett is a Senior Economist, Catherine Birch is a Senior Economist, Adelaide Timbrell is an Economist, Hayden Dimes is a Market Economist and Jack Chambers is a Rates Strategist at ANZ

This is an edited version of an ANZ Research report

Share

Related articles

-

The $US is shifting form, and recent depreciation is likely to be the new normal.

2025-06-18 00:00 -

A new approach to asset financing is building equity in First Nations suppliers to the mining industry. First Nations procurement targets in other industries could be met with a similar approach.

2025-06-10 00:00 -

The road to normalisation in the world’s largest bilateral trading relationship looks complex.

2025-05-28 00:00

This publication is published by Australia and New Zealand Banking Group Limited ABN 11 005 357 522 (“ANZBGL”) in Australia. This publication is intended as thought-leadership material. It is not published with the intention of providing any direct or indirect recommendations relating to any financial product, asset class or trading strategy. The information in this publication is not intended to influence any person to make a decision in relation to a financial product or class of financial products. It is general in nature and does not take account of the circumstances of any individual or class of individuals. Nothing in this publication constitutes a recommendation, solicitation or offer by ANZBGL or its branches or subsidiaries (collectively “ANZ”) to you to acquire a product or service, or an offer by ANZ to provide you with other products or services. All information contained in this publication is based on information available at the time of publication. While this publication has been prepared in good faith, no representation, warranty, assurance or undertaking is or will be made, and no responsibility or liability is or will be accepted by ANZ in relation to the accuracy or completeness of this publication or the use of information contained in this publication. ANZ does not provide any financial, investment, legal or taxation advice in connection with this publication.