-

Published April 22 2021

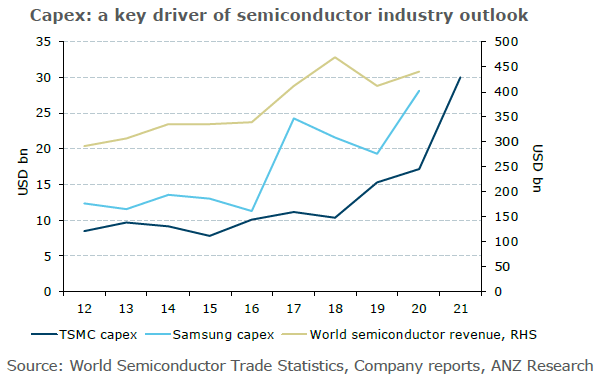

The capex plans of leading semiconductor companies around the world suggest there is life left in the current tech cycle upswing.

Tech giant Samsung’s capital expenditure rose a massive 45 per cent year-on-year to $US28.1bn in 2020, and industry analysts believe this expenditure will continue through 2021.

Taiwan Semiconductor Manufacturing Company (TSMC) has unveiled a multi-year ramp-up in capex plans, lifting its 2021 capex estimate to $US30 billion. This is part of TSMC’s three-year plan to invest $US100 billion towards chip fabrication capacity expansion.

These two leading producers are likely to account for nearly 43 per cent of worldwide semiconductor industry capex, according to an IC Insights report.

Demand for tech has seen robust growth. Mainland China has emerged as the largest market for new semiconductor equipment, with sales growth of 39 per cent year on year to $US18.7 billion. It outpaced Taiwan ($US17.2 billion) and South Korea ($US16.1 billion) to top the global chip manufacturing equipment market for the first time in 2020.

A shortage of semiconductor chips is also impacting demand-supply dynamics. Industry leaders believe the ongoing semiconductor chip shortage is likely to remain until 2022. Executives at both Intel and TSMC have also alluded to the shortage persisting as demand outstrips supply.

The scale-up in capex comes amid a backdrop of robust tech demand and a shortage of semiconductor chips. As capacity ramps up, Asia’s tech economies are likely to feel the tailwinds in their export demand.

Bansi Madhavani is a Senior Economist at ANZ

This story is an edited version of an ANZ Research report. You can read the original report HERE.

Share

Related articles

-

Potential disinflationary effects would be balanced by a reduction in export competitiveness, ANZ Research suggests.

2026-04-01 00:00 -

A sharp lift in IT capital expenditure signals an expectation AI utilisation in Australia will increase.

2026-03-19 00:00 -

In many ways the economic impact of the latest events propagates the trends of recent years, ANZ’s Chief Economist says.

2026-03-19 00:00

This publication is published by Australia and New Zealand Banking Group Limited ABN 11 005 357 522 (“ANZBGL”) in Australia. This publication is intended as thought-leadership material. It is not published with the intention of providing any direct or indirect recommendations relating to any financial product, asset class or trading strategy. The information in this publication is not intended to influence any person to make a decision in relation to a financial product or class of financial products. It is general in nature and does not take account of the circumstances of any individual or class of individuals. Nothing in this publication constitutes a recommendation, solicitation or offer by ANZBGL or its branches or subsidiaries (collectively “ANZ”) to you to acquire a product or service, or an offer by ANZ to provide you with other products or services. All information contained in this publication is based on information available at the time of publication. While this publication has been prepared in good faith, no representation, warranty, assurance or undertaking is or will be made, and no responsibility or liability is or will be accepted by ANZ in relation to the accuracy or completeness of this publication or the use of information contained in this publication. ANZ does not provide any financial, investment, legal or taxation advice in connection with this publication.