LIBOR Transition Customer Frequently Asked Questions

(May 2020)

These Frequently Asked Questions (FAQ) should be read in conjunction with ANZ’s “LIBOR Transition Customer Presentation”. This presentation is available through your ANZ representative.

ANZ believes the information contained in these FAQs to be accurate as at the date on the cover page. ANZ is not obliged to update the information or notify any person should any information contained in these FAQs cease to be correct. The information contained in these FAQs is high level and intended a summary only and should not be relied on as being current, complete or exhaustive. This information has not been prepared specifically for you or taking into account your particular circumstances.

The information is not intended in any manner, and should not be interpreted, as ANZ providing advice to you. LIBOR Transition is a constantly evolving topic, and this means information quickly becomes out of date. Make sure you keep yourself up to date and informed on transition issues using current information.

The contents of these FAQs have not been reviewed by any regulatory authority.

The London Interbank Offer Rate (LIBOR) is known as the “most important number in the world”. It underpins about USD400 trillion worth of financial contracts globally, ranging from complex derivatives to home loans and credit cards. Despite once being the most important number in the world, LIBOR is on the way out. From the end of 2021, LIBOR is expected to become part of financial market history. How, you might ask, can such a vital rate stop being available? What rate will be used instead? What does this change mean for you? These FAQs set the scene and provide some background to the transition away from LIBOR.

Derivatives in Other Currencies

Operationalising the Derivative Fallbacks

Pre-cessation Triggers

Cross Currency Derivatives

Credit Support Annexes

Loan Fallbacks

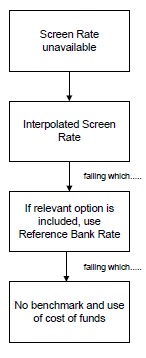

Because there is a lack of industry standard documentation across lending products, fallback provisions vary from deal to deal, and some contracts may not contain fallback provisions at all. Where they are included usually the waterfall of fallbacks is as follows:

Generally existing loan fallbacks only apply when a rate becomes temporarily unavailable (the “Screen Rate” being the relevant benchmark rate).

The market recognises legacy fallback options were not intended to cater for a permanent cessation scenario. In particular, because the fallbacks themselves are based on LIBOR rates they do not work once LIBOR is permanently discontinued and replaced by a rate that is calculated on a different methodology entirely. Existing fallbacks also do not include the ability to adjust credit spreads to “re-balance” the economic equation.

Provisions have been included in loan contracts to accommodate LIBOR cessation.

- Screen Rate Replacement language. The European Loan Market Association (LMA) and the Asia Pacific Loan Market Association (APLMA) published the so-called “replacement of screen rate” rider for insertion into primarily syndicated and club agreements.

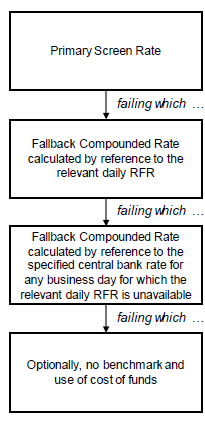

- LMA’s Exposure Drafts. The LMA has published exposure drafts of single-currency facility agreements for sterling and US dollars with pricing based on RFRs (SONIA/SOFR) calculated on an in arrear basis with a “lag” period. These drafts do not provide fallback language for existing LIBOR deals, but are intended to facilitate discussions about how new deals based on RFRs will be documented and priced. The proposed rate waterfall in the exposure drafts is as follows:

The clauses in the rider do not include alternative fallback rates, but are intended to serve as an acknowledgement between the parties that if a benchmark rate cessation trigger event occurs (for example, the benchmark is discontinued or is no longer deemed to be representative or appropriate for calculating interest), the parties will agree an alternative benchmark rate and make the necessary changes to the contractual arrangements, and to the economics of their transaction, to implement it.

In syndicated loans, the provisions are also intended to simplify the amendment process by lowering the consent threshold. ANZ has been incorporating “replacement of screen rate” provisions into new and amended lending documents since late November 2018.

The “Primary Screen Rate” is essentially an externally produced compounded average of the RFR made available by an information provider. There is currently no Primary Screen Rate for any LIBOR currency.

The LMA is requesting feedback from the market on commercial issues raised in the drafts and commentary document accompanying them, and ANZ will be monitoring any published responses or the LMA’s observations from feedback received on the drafts.